Introduction

You applied for life insurance expecting a straight yes-or-no answer. Instead, you got a decline, a much higher premium than expected, or a notice telling you to try again later. That happens more often than you’d think, especially if you have a medical history, hazardous work, or specialized hobbies.

Many agents only have a few standard carriers to work with, so once those options say no, the process can stop there. In many high-risk life insurance cases, though, that is not the end of the market — it is just the end of the standard market.

What Is Impaired Risk Life Insurance?

Impaired risk life insurance is not a special policy type sitting on a separate shelf. It is an underwriting category insurers use when an applicant presents a higher-than-average level of risk based on health, occupation, or lifestyle.

That higher risk can come from several places:

- A prior heart attack or ongoing cardiac condition

- Type 1 or Type 2 diabetes

- Cancer treatment history

- Obesity

- Depression or anxiety treatment

- Hazardous occupations

- Activities like private aviation or scuba diving

In other words, this is simply life insurance for higher-risk individuals whose file needs closer review than a standard healthy applicant.

High Risk vs. Uninsurable: They Are Not the Same Thing

This distinction matters.

Some high-risk life insurance companies decline broad categories because their underwriting guidelines are narrow. Other high risk life insurance carriers are willing to issue coverage at a higher premium if the applicant’s condition is stable, well documented, or far enough in the past.

The question is often not “can you get insured?” but “which carrier is willing to review your case differently?” That is a very different conversation from filling out another generic online quote form.

Why Standard Brokers Run Out of Options

When you’re denied life insurance, it’s easy to assume every company would have said the same thing. In reality, many general brokers regularly work with only a small group of mainstream carriers, often 3 to 5. Those carriers often focus on more straightforward underwriting, and they may have less flexibility for higher-risk profiles.

That means if your file falls outside those carriers’ guidelines, the broker may simply run out of places to submit it within that limited market.

This is not always because the broker did something wrong. It is often because their available market is limited to the carriers they can access.

The Difference Between a General Broker and an Impaired Risk Specialist

A standard broker may submit applications through a similar process regardless of complexity. An impaired risk specialist reviews the details first and focuses on carriers that are more likely to consider your specific profile.

That difference matters because impaired risk life insurance carriers don’t all view the same condition the same way.

For example, someone declined by a standard term carrier may still receive a table-rated offer through a broader underwriting market that considers managed diabetes, cardiac history, or a prior cancer remission, depending on the full medical file and the carrier’s guidelines. The offer may come back at a higher premium rather than preferred pricing, but having coverage can be meaningfully different from having no coverage at all.

Common Conditions That Trigger High-Risk Life Insurance Underwriting

Many people start here with a simple question: “Does my situation count as high risk?” In most cases, it depends less on one diagnosis label and more on the full underwriting picture, timing, severity, treatment, and current stability.

Medical Conditions Underwriters Often Review Closely

Some of the most common medical triggers include:

- Heart attack history

- Coronary artery disease

- Atrial fibrillation

- Diabetes

- Obesity

- Multiple sclerosis

- Epilepsy

- Parkinson’s disease

- Cancer history

- Depression, anxiety, or bipolar disorder

What matters is not just the name of the condition.

Underwriters usually look at:

- when the diagnosis occurred

- whether treatment is ongoing

- whether the medication is stable

- whether follow-up care is consistent

- and whether symptoms are controlled

For example, cancer treatment completed three months ago is evaluated very differently from cancer in remission for two years. Controlled diabetes with consistent follow-up and stable labs is evaluated differently from uncontrolled diabetes with an inconsistent lab history.

This is why many high-risk life insurance applications need more than a simple yes/no underwriting screen, and why the details in your file matter.

Occupations and Hobbies That Raise Underwriting Flags

Not every impaired-risk file is tied to health.

Applicants can also face added underwriting review because they are:

Occupations

- Pilots

- Firefighters

- First Responders

- Offshore workers

- Commercial Divers

- or involved in physically dangerous environments

The same applies to hobbies such as:

- Scuba diving

- Rock climbing

- Private aviation

- Motorsports

These are not medical conditions, but they still affect mortality assumptions. Some high-risk life insurance carriers have much stricter internal thresholds for these exposures than others, which again makes carrier selection important.

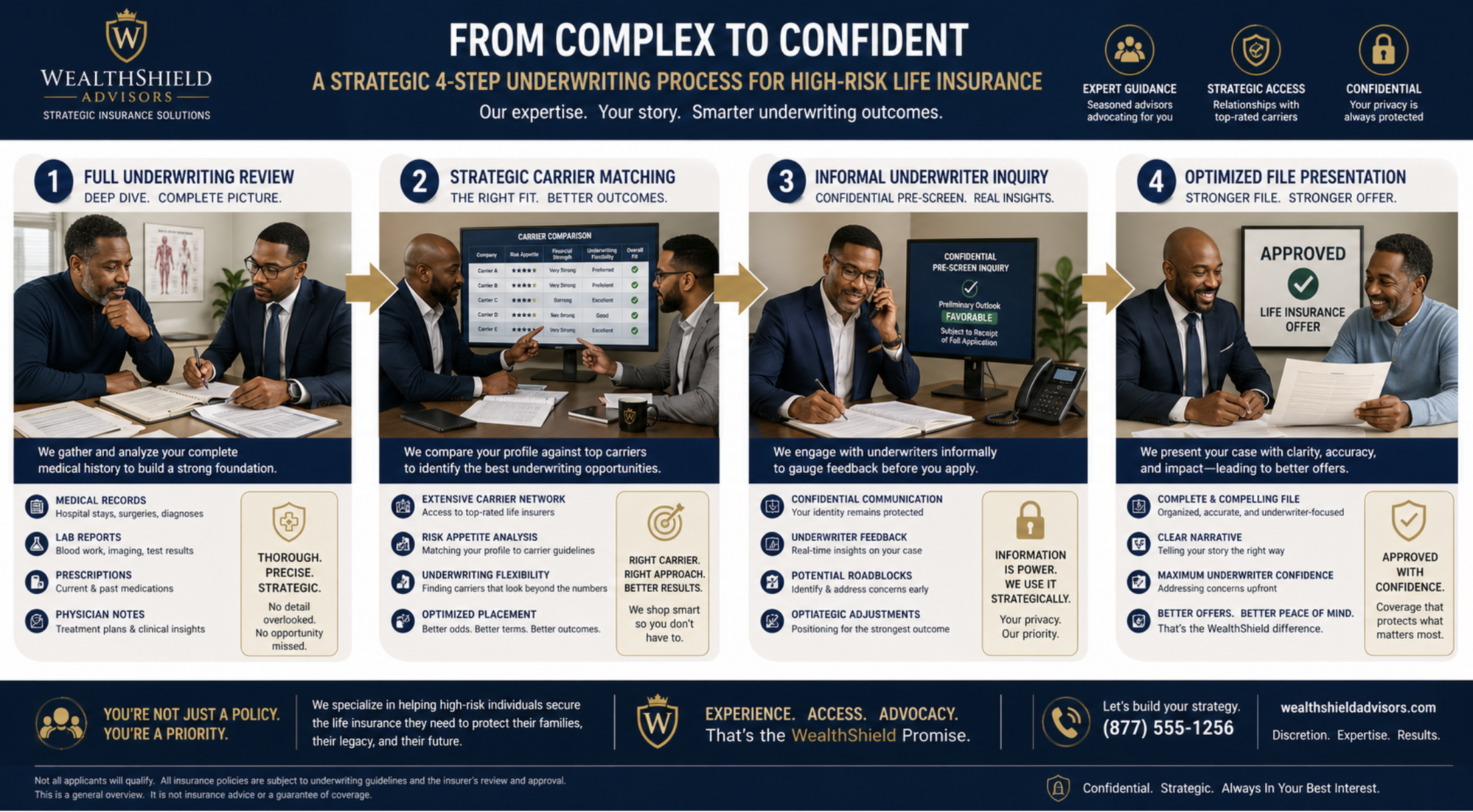

How the Impaired Risk Life Insurance Process Works

A specialist approach usually follows a more deliberate process than submitting multiple online applications without a clear underwriting plan.

Full Underwriting Review Before Shopping

The first step is gathering the complete picture:

- diagnosis dates

- medications

- physician notes

- recent lab trends

- occupation details

- and lifestyle disclosures

Incomplete disclosure can lead to delays and inconsistent underwriting outcomes. If an underwriter receives partial information, they may interpret the risk more conservatively, and the result can come back less favorable than it otherwise might.

Match Your Case to the Right Carriers

Not every carrier should see every file.

This is where advisors with impaired-risk experience review which high-risk life insurance carriers are more likely to consider your specific combination of facts.

Some may be more open to controlled metabolic issues. Some may be more flexible on cardiac history after a waiting period. Others may be more responsive to occupational risk than medical risk.

That means applications are often sequenced with purpose rather than sent out broadly.

Use Informal Inquiries When Needed

In more complex cases, a specialist can approach underwriters informally before submitting a full formal application.

This can help test whether a carrier is likely to consider your case, gather preliminary feedback, and reduce the chance of unnecessary formal applications, depending on the carrier’s process.

For someone who has already been denied life insurance, this can help you focus on the next steps and avoid repeating the same submissions.

Present the File the Right Way

How information is presented can affect how underwriting is evaluated.

Stable treatment history, improved labs, physician compliance, time since a medical event, and documented lifestyle changes can all shape how a carrier views the overall risk. A controlled diabetic applicant with a strong A1C history is not presented the same way as an applicant with recent uncontrolled readings.

This is one of the reasons life insurance for high-risk individuals is often a file review process, not just a quote request.

If you’ve already been declined once, a specialist review before another application can help you avoid unnecessary submissions, depending on the facts of your case.

Rated Policy, Table Rating, Postpone, or Decline: What to Expect

Underwriting results do not always come back in plain language, which can leave you unsure whether you received bad news or a result you can still work with.

Rated Policy

Rated policies mean you are approved, but at a higher premium than a standard applicant, because the insurer sees added risk.

This still means coverage exists. If you’re reviewing high-risk life insurance quotes, it can help to know that a rate above standard pricing is not the same as a rejection.

Table Ratings Explained

Most carriers express non-standard approvals in table ratings.

The higher the table, the higher the additional cost tied to underwriting risk.

That does not automatically mean those rates stay at the same level indefinitely. In some impaired risk life insurance situations, you may be able to request reconsideration later if health markers improve or more time passes after treatment, depending on the carrier’s rules.

Postponed vs. Declined

Postponed means the carrier is saying “not now.” They may want to see more time after surgery, more time after cancer treatment, or more stable physician follow-up.

Declined means that the carrier will not issue coverage under its current guidelines.

Neither response means the entire market is closed. In some cases, it means a different carrier may need to review the file based on its own underwriting approach.

This is where many applicants stop after one or two answers. In some cases, the issue is that the first carrier was not a good fit for the facts of the case.

Why Working With Liberty One Matters If You’ve Been Denied

If you’ve been denied life insurance, working with Liberty One can help you take a clearer, more structured next step. Instead of restarting with the same basic application path, we start by reviewing what drove the decision and what information the carrier used.

We look for where the underwriting friction is coming from and which carriers are worth approaching next, based on your facts. That can be useful when you’re comparing high-risk life insurance companies and trying to understand whether the outcome was carrier-specific or more likely to repeat across similar underwriting guidelines.

We also explain the tradeoffs in plain language. If a table-rated offer is the most workable option right now, we’ll walk through what the rating means and what it does (and doesn’t) change about the coverage. If a carrier postpones a decision, we’ll explain what “postpone” typically means and what information or timeframes a carrier may want to see before reconsidering, depending on the carrier. The goal is clarity, so you understand where your case stands and what your options look like before you submit another application.

Frequently Asked Questions

Common questions about high-risk and impaired risk life insurance

The most common triggers include cardiovascular issues (such as a prior heart attack or atrial fibrillation), metabolic conditions (such as diabetes or obesity), cancer history, neurological disorders, and mental health diagnoses. Occupations such as firefighting, offshore work, and aviation, as well as hobbies like scuba diving or motorsports, can also lead to a higher-risk underwriting review. The important part is this: these factors often lead to stricter underwriting, but they do not automatically mean you are uninsurable.

Yes, a denied life insurance application from one company doesn’t automatically mean every carrier will give you the same answer. Many mainstream brokers only shop a small group of carriers (often 3 to 5), while specialist markets include additional high-risk life insurance carriers that may review your file differently and offer a rated policy (a higher premium) instead of a flat decline, depending on your situation and the carrier’s guidelines.

In more complex cases, an impaired risk advisor can also use informal underwriting inquiries before sending another full application, which can help reduce unnecessary formal applications and focus on carriers that are more likely to consider your profile.

A table-rated policy means you’re approved for coverage, but at a higher premium because the carrier sees added risk. For example, Table 2 is often described as about 50% above standard rates, while Table 4 is often described as about 100% above standard, though the exact pricing and tables vary by carrier.

Many applicants looking for high-risk life insurance quotes assume this is a rejection, but a table rating is still an approval, just at adjusted pricing. In some situations, a carrier may reconsider the rating later if your health profile changes or more time passes, based on the carrier’s guidelines.

A regular broker often submits your case to a small group of standard carriers and waits for a decision. An impaired risk specialist works differently by focusing on carriers with non-standard underwriting and matching your file to the carriers that may be more likely to consider your specific health history, occupation, or lifestyle factors.

Just as important, a specialist may use informal inquiries in some cases, so you can get a clearer sense of a carrier’s interest before submitting a full application. They also help present the medical details clearly and consistently, and avoid sending the same file to carriers that are unlikely to be a fit based on their guidelines.

Denied Does Not Mean Done

A denied life insurance application or being rated up does not always mean your options are gone. In many high-risk life insurance cases, the difference comes down to which carriers you approach, how complete your medical and lifestyle file is, and understanding how underwriters evaluate your specific situation.

Liberty One works with individuals and families who want a clear review of what happened and what to consider next, beyond a standard quote engine. If you’d like to talk through your situation, you can speak with a Liberty One advisor and start with a straightforward conversation.